Alliance Bank 2 for 17 Rights Issue to raise RM602 million

Four-Day Declines and what History SaysSince the Reciprocal Tariffs announcement by Trump on 2/4/25, this was how the S&P 500 ended:

2/4/25 – 5670

3/4/25 – 5396

4/4/25 – 5074

7/4/25 – 5062

8/4/25 – 4983

a loss of 12.1% in the 4 days following the announcement and a drop of 19% from its peak of 6147 in Feb 2025.

Based on data collected by Creative Planning Chief Market Strategist Charlie Bilello, the S&P 500 has endured 15 Four-day Declines of 11.5% to 28.5% between 1950 and 2025. This period saw dramatic falls during the Black Monday crash of 1987, the Global Market Collapse of 2008, and the 2020 COVID pandemic crash. In these scenarios, the analyst worked out that the total returns (including dividends) of the S&P 500 at the one, three and five-year periods following each of these four-day declines were always higher than the total decline at the time.

Source: Yahoo Finance

Ken Fisher weighs in on Recession OutlookBillionaire investor Ken Fisher (who is the son of Phil Fisher*) weighed in on the possibility of a recession this year with his dismal outlook if tariffs aren’t rolled back following the 90-day pause in reciprocal tariffs.

“If it does not resolve that President Trump and crew have negotiated some deals and then put all of this nonsense behind us, or 90% of all this nonsense behind us, you’ll see a very bad economic effect that will cause a recession, and it will be recession before the end of the year.”

While it’s too early to declare a recession, Fisher was quoted as saying:

“We never get a recession unless the US stock market and global stock market have peaked from an all-time high and gone down for three or fourth months,” said Fisher. “It won’t start any sooner than that.”

Source: The Street

* Phil Fisher, the author of “Common Stocks and Uncommon Profits” is credited as the father of value investing and widely revered by investment legends such as Warren Buffett.

US Investors to Offload US$800 billion of China Equities?Anything can happen in an escalating trade war between US and China. According to Goldman Sachs. US institutions currently hold some $250 billion or 26% of total Chinese ADRs while their Hong Kong stock holdings amount to $522 billion. Together with their holding of China A Shares, total exposure of some $800 billion. In the extreme scenario of financial separation between the two countries, US investors could potentially be forced to divest of their investment holdings in China equities.

Source: Times of India

Escalating Trade Tension to lift China’s demand for Palm OilThe escalating trade tension between US and China will likely further reduce China’s soybean imports dependency on the US by diverting part of its soybean imports to South America. This will benefit Brazil and Argentina, the world’s largest and third largest soybean producing countries. It may also result in replacement of China’s soybean demand to palm oil as a substitute.

What happened during the first US-China tariff tension in 2018?

Recall, China’s move to impose a 25% tariff on US soybean imports in retaliation against US tariffs) had resulted in China’s soybean imports from US declining by 57% (or 18.6m metric tons) in 2018. During the same time, its soybean imports from Brazil rose by 41% (or 21.8m metric tons) and resulted in China’s palm oil imports increasing by 5% to 5.3m metric tons.

Tariffs have muted impact on US palm oil demand

The impact of US tariff on America’s palm oil demand, on the other hand, will likely be muted. In 2024, US imported a total of 1.8m metric tons of palm oil, mostly from Indonesia.

Source: HLIB Research 17/4/25

Canada and Japan big buyers of Treasuries in FebruaryAgainst the backdrop of the current US Treasury sell off, it is interesting to note that Canada and Japan were among the biggest net buyers during the preceding month. Foreign holdings of Treasury securities hit a high of US$8.82 trillion in February. Here’s a tally of the large foreign holders:

Japan $1.13 trillion

China $784.3 billion

UK $750.3 billion

Belgium US$394.7 (include Chinese custodial accounts)

The foreign holdings for April will only be revealed in June, giving more clarity over any weaponization issue and strategy via US Treasuries.

The US Treasuries SelloffThere are trade war theories that China is weaponizing their US Treasury holdings although some analysts disagree as the sell down may necessitate capital being moved back into China causing yuan appreciation. Others say that China can also convert the proceeds into Euros or German bunds. May explain Germany’s bunds bucking a wider sell-off in long-dated Treasuries last week. Other theories point to Japan’s life insurers selling due to concerns about US policy flip-flops, while others say it is the Hedge Funds and Bond Vigilantes.

Source: CNBC

Rare Event could send S&P 500 tumbling againWhen the 50-Day Moving Average crosses below the 200-Day Moving Average, some chartists see this signal as a turning point known as a “death cross.” The S&P 500 suffered its first death cross since 2022 this week whereby investors can potentially suffer substantial short-term losses.

Source: TheStreet

Banking Shares expected to stay Rangebound pending trade clarityNotwithstanding the current trade war climate, CIMB Research does not believe that the price-to-book valuations of banking stocks will fall to the COVID-19 lows of 0.3 to 0.5x Book Value. During the pandemic lockdown, 70% to 80% of loans were placed under moratorium in the initial phase, before dropping to 30% on an opt-in basis towards the end of 2020. However in the current scenario, loan relief assistance can be more targeted towards exporters and affected companies in the supply chain, making the current uncertainty less widespread as compared to the pandemic days.

Source: TheStar

With a tariff trade war, US will obviously feel pain from goods inflation and slowing economy from job losses. What about China?China’s GDP in 2023 was $18 trillion. It exported goods to the US worth US$440 billion (less than 2.5% of its GDP). Furthermore China only imported around US$150 billion worth of goods from the US. So why should it be concerned? Here’s the answer according to Google Gemini:

1. The Absolute Value and Contribution to Growth:

While the percentage might seem small, the absolute value of exports to the U.S. is still enormous (hundreds of billions of dollars). This contributes significantly to China’s export revenue, which has historically been a major driver of its economic growth and employment. Even a small percentage of such a large GDP translates to a substantial impact when lost or reduced.

2. Interconnectedness of Supply Chains:

A significant portion of China’s exports to the U.S. are intermediate goods and components that are part of complex global supply chains. Tariffs on these goods can disrupt these chains, impacting not only Chinese manufacturers but also U.S. businesses and consumers. Disruptions can lead to decreased efficiency, increased costs, and the need for companies to find alternative suppliers, potentially leading to a longer-term shift away from China.

3. The U.S. Market’s Importance:

The U.S. is a major consumer market with significant purchasing power. Access to this market has been crucial for the growth and development of many Chinese industries.

Losing or facing restricted access to the U.S. market can limit the growth potential of these industries and force them to find alternative markets, which may not be as large or as profitable.

4. Signaling Effect and Future Uncertainty:

U.S. tariffs and trade policies can create uncertainty for Chinese businesses regarding future trade relations. This uncertainty can deter investment, impact long-term planning, and encourage diversification of supply chains away from China by other countries and companies.

Even if current tariffs only affect a small portion of GDP, the potential for further escalation and broader restrictions is a significant concern.

5. Impact on Specific Sectors and Employment:

While the overall GDP impact might be small, certain sectors in China are heavily reliant on exports to the U.S. Tariffs can have a significant impact on these specific industries, leading to job losses and economic disruption in those regions. Examples include electronics, machinery, textiles, and toys.

6. Trade Balance and Currency Issues:

The large trade surplus China has with the U.S. has been a point of contention. U.S. tariffs are often aimed at reducing this trade deficit. While the overall GDP impact might be limited, changes in the trade balance can have implications for currency exchange rates and China’s foreign exchange reserves.

7. Geopolitical Implications:

Trade issues are often intertwined with broader geopolitical tensions. China is concerned that U.S. trade policies are part of a larger strategy to contain its economic and technological rise.

In summary, while the direct percentage of China’s GDP from exports to the U.S. might appear small, the absolute value, the interconnectedness of supply chains, the importance of the U.S. market for specific sectors, the potential for future escalation, and the broader geopolitical implications all contribute to China’s significant concern regarding U.S. trade policies and tariffs. The impact goes beyond just a simple percentage of GDP.

Source: Google Gemini

More Reading: List of Top Products exported by US to China

When does History say Stocks might Recover after a Market Crash?2020 COVID-19 Market Crash

S&P 500 dropped almost 14% over two days on 11 and 12 March, bottoming out on 23 March, with declining another 10% making a total decline from peak of around 34%. This was a steep yet quick fall with a fast recovery due to Fed intervention.

2008 Subprime Mortgage Crisis

S&P500 declined by 8.8% on 29 Sep and later declined by about 20% the week of Oct. 6. The market found a bottom five months later in early March 2009 losing another 44% after the initial plunge on 29 Sep. The S&P500 lost more than half its value during the five month bear market and took more than five years for the market to return to new highs. The Fed slashed interest rates to near zero percent and initiated QE.

1987 Black Monday

The DJIA lost 22.6% on 19 Oct as a result of to overvaluation and speculation. It reached a second bottom in early December and took nearly two years to reach new highs. The crash was a valuation reset after a long bull market.

1929 Wall Street Crash

The Dow Jone plunged 23% over a two-day period in late October resulting from runaway speculation and high valuations. Several tough followed as the DJIA would decline another 82% before reaching a bottom in July 1932. The Dow’s peak to trough decline was 89% and it took 25 years for the market to fully recover.

Source: Motley Fool

US Treasury sees modest pickup in customs duties amid widening deficitThe US Treasury received US$9.0 billion of customs revenue for March, a US$2.0 billion increase from 2024. The federal deficit hit US$1.31 trillion in six months, up 15% from a year earlier.

Source: AHIB

Credit Markets ParalysedCompany debt sales have ground to a halt in the US following Trump’s escalating trade war and fears of a global recession. Several leveraged loan sale and debt refinancing have been put on hold and no new US investment-grade bonds have been issued since Wednesday 2/4/25. Transactions on riskier debt are being pulled or postponed, while perceived risk for high-grade and high-yield US corporate bonds are flashing warning signs.

Source: The Star

Audi holding cars in U.S. ports due to autos tariffCarmakers on average have just under three months’ worth of inventory on hand in the United States, according to data from automotive services provider Cox Automotive, giving them some breathing room to keep supply intact until they establish a longer-term strategy for dealing with the tariffs.

Source: Reuters

The DJIA index fell 22.6% on Monday 19 October 1987, plunging 508 points to 1738. In the wake of Trump’s tariff war announced on 2/4/25, a similar percentage fall on Monday 7/4/25 would have taken 8,000 points off the DJIA. As it turned out, Monday was relatively calm following Thursday’s 5% drop and Friday’s 6% drop.

Source: 247 Wallst

US imports a lot more goods from China (US$439.7 billion) than it exports (US$144.6 billion).

Soybeans, oilseeds and certain grains were a key US export to China, amounting to US$13.4 billion last year. And China bought 52% of US soybean) exports in 2024.

Source: Malay Mail

Nike stock price rallied 4% after Trump’s post that he had a call with Vietnam’s To Lam. About 25% of Nike’s footwear is made in Vietnam. Nike is also one of the biggest holdings of Ackman’s portfolio. On 28/6/24, it reported sales that missed analyst estimates. The stock fell 20%, its biggest one-day drop since 1980. Nike’s stock price had tumbled 30% in 2024.

Source: The Street

Trade war will result in China moving towards alternative agriculture suppliers including Brazil. China is imposing additional duties of 34% on all US goods (on top of the 10%-15% tariffs) placed on US$21 billion worth of agricultural products, effectively closing doors on all US agricultural imports. The main impact will be on products like soybeans and sorghum, not so much on wheat and corn as China has not been buying much of wheat and corn from the US in 2025. EU is likely to put tariffs on US soybeans, leading to product substitution to others such as palm oil.

Source: The Edge

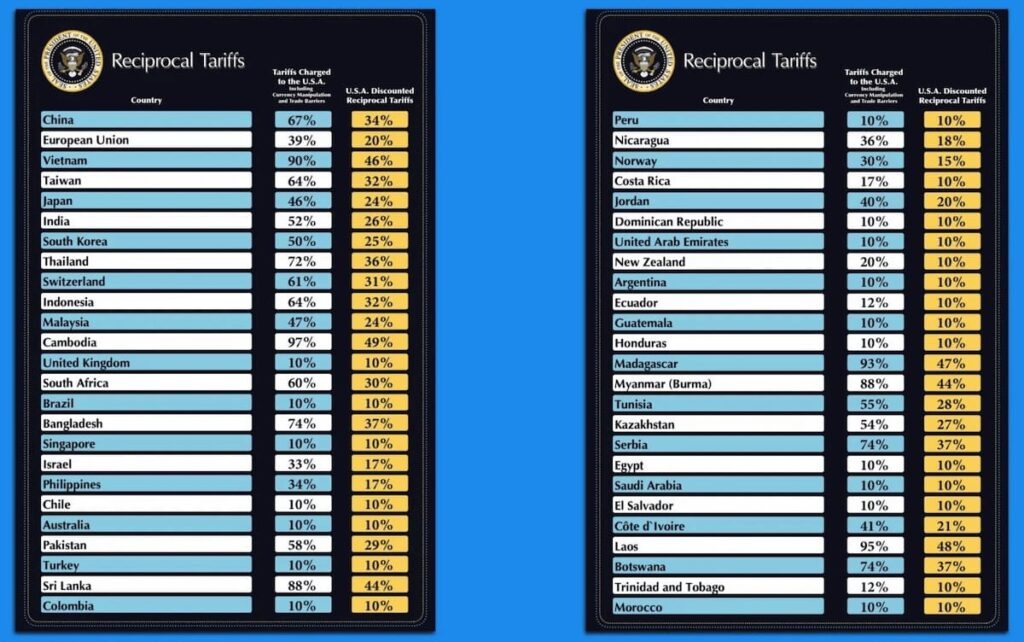

“Liberation Day” Tariffs Explained

1. Trump’s (特离谱) All-Out Tariff Strategy

Trump’s “global tariff” plan is not primarily aimed at fixing trade deficits or reshoring manufacturing. It is a geopolitical and financial maneuver to force all countries to bear the cost of U.S. debt—a move to “leverage U.S. market access to coerce foreign cooperation.”

2. The Real Crisis: U.S. Sovereign Debt

As of early 2025: Debt: $36 trillion+

Annual tax revenue: $5 trillion

Annual spending: $6.75 trillion

Debt interest: $1.12 trillion

This creates a dangerous debt spiral: deficit → borrow more → pay more interest → deeper deficit.

3. August 2025 Deadline: The Ticking Bomb

Debt ceiling set at $36.1 trillion.

U.S. Treasury using emergency measures to avoid breaching the cap.

Come August–September 2025, funds will be exhausted unless the cap is raised.

Source: Unknown

More Reading: Raise Money Now, Cut Taxes Later

4. Need for $6 Trillion in 2025

To stay afloat in 2025, the U.S. needs to raise:

$3 trillion (for maturing bonds)

$1.12 trillion (for interest)

$2 trillion (budget deficit)

=> Need total of $6 trillion in new debt

The market may not be able to absorb such volume, threatening the collapse of the U.S. Treasury market and dollar credibility.

5. Trump’s Initial Moves

Budget cuts: $2 trillion

Cut foreign aid (e.g., Ukraine), sell immigration “green cards”

Created “Department of Government Efficiency” led by Elon Musk (which failed)

These actions hint at an impending fiscal cliff, and tariffs are just phase one of a larger plan.

6. Conclusion

Tariffs won’t raise $6T before August 2025.

Trump is forcing countries to indirectly pay by buying U.S. debt.

Expect further escalation if countries resist.

The goal: Avoid default, preserve dollar hegemony, and control inflation without expanding the Fed’s balance sheet.

A steep correction could be in store for gold price according to Morningstar’s Jon Mills. There are long-term trends that could push bullion back to $1,820. Current high price and margins are encouraging greater production and exploration. Global central banks purchased a net 1,045 tons of gold through 2024, the third straight year of purchases over 1,000 tons. Inflows into Gold ETFs reached $9.4 billion in February, the highest inflow in nearly three years (World Gold Council data). But there are signs that the world’s appetite for gold is starting to wane. In a survey by WGC last year, 71% of central banks said they expected their own gold holdings to remain the same or decrease in the coming 12 months. Also investor appetite will likely dip, given that economic concerns are typically only short-term factors influencing gold prices: Eg Gold price briefly spiked in 2020 in response to pandemic fueled concerns. But price fell quickly thereafter and didn’t reach the prior peak until late 2023.

Source: Yahoo Finance

Foreign investors extended their selling streak on Bursa Malaysia for the 22nd consecutive week, with a net outflow of RM1.25 billion. Foreign ownership in Malaysia Treasury Bills in Feb 2025 stood at 52.7%, while Bank Negara Malaysia’s international reserves stood at US$118 billion.

Source: The Edge

According to BoA, S&P500 could see 12% drop to 5000 in a downturn with increased unemployment, then increase to 5500 to end 2025. At the time of publication (EOD 27/3/25), S&P500 closed at 5712 and tumbled to 5074 at EOD 4/4/25 in response to Trumps’ Liberation Day tariff announcement on 2/4/25.

Source: Business Insider

Vietnam will cut its tariffs on several U.S. products including LNG and cars, and moved to approve Starlink services, as the country tries boost US imports and avoid being hit with U.S. tariffs because of its trade surplus which exceeded $123 billion last year. Under the new plans, the tariff on American LNG will be cut from 5% to 2%, automobiles from a range of 45% to 64% to 32% , and on from 10% to 5%.

Source: Reuters

Malaysia’s IPO sentiment has cooled significantly since 20/2/25, despite strong subscription rates.

Source: New Street Time

Alliance Bank Rights Issue to raise up to RM600 million

Alliance Bank is seeking to raise as much as RM600 million in fresh capital via a rights issue of new shares to fund its general banking, financing and investing activities. Alliance Bank’s share price closed at RM5.09 on 21/3/25, gaining around 50% over the past 12 months and giving it a market capitalisation of RM7.87 billion. The rights issue is expected to be completed by the third quarter of 2025 and is subject to regulatory and shareholder approvals.

Source: TheEdge

It opened 17% lower at 73sen and closed at 83sen, making it the third listing to close below IPO price in 2025.

Source: TheEdge

According to JP Morgan Chase, the $5.5 trillion S&P 500 correction was most likely driven by two types of equity hedge funds adjusting their positions rather than investor concern about a potential recession: Quant hedge funds & TMT sector hedge funds. Quant hedge funds typically use data and code to make investment decisions, while TMT sector hedge funds primarily invest in firms related to technology, media and telecommunications. Bank of America said S&P500 has more downside potential before reaching a price floor while Morgan Stanley said S&P500 is now hovering at an area where it could ignite tactical rallies, saying that 5,500 should provide support for a tradable rally led by cyclicals, lower quality, and expensive growth stocks that have been hit the hardest and where the short base is the greatest. As it turned out, the recent falls from 3/4/25 to 8/4/25 were much more severe than anyone expected.

Source: Daily Hodl

US imposed a 25 percent tariff on virtually all goods produced by their two top trading partners — Canada and Mexico. At the same time it also imposed a 20% tariff on all China goods. As a result, the average tariff level is now higher than at any time since the 1940s. China and Canada immediately retaliated.China hit back with a 15 percent tariff on American agricultural products and the Canada putting a 25 percent tariff on $30 billion of US goods. Mexico vowed retaliatory tariffs.

Source: Vox